Green Property Certificate in Punjab: What Buyers and Sellers Need to Know

Learn how the Green Property Certificate in Punjab will replace Fard, reduce property fraud, and become mandatory for property transfers in 2026.

Key Takeaways

The Punjab government has introduced the Green Property Certificate (GPC) to replace the traditional Fard for property transactions. Piloted in Sahiwal from May 1, 2026, the GPC is linked to the provincial computerized land records and will be mandatory for all transfers from December 2026. The process includes identity verification, payment of a nominal fee (around Rs. 950), and online integration with the Punjab land registry. Property owners and prospective buyers should verify GPC status as part of transaction due diligence.

Quick Facts Table

Policy

Green Property Certificate (GPC) replacing Fard

Pilot start

May 1, 2026 (Sahiwal district)

Mandatory from

December 2026 (for all property transfers in Punjab)

Purpose

Digitize land records, reduce fraud, enhance verification

Application fee

Nominal, around Rs. 950 (as per available information)

Identity verification

NADRA or government-issued IDs; verification integrated online

Payment channels

Designated banks (e.g., Bank of Punjab) and online payment methods

Record integration

Linked with Punjab’s computerized land records (MPDC system)

Introduction

Punjab’s Green Property Certificate (GPC) represents an administrative shift toward digital property records. According to official roll-out information, the GPC replaces the traditional Fard as the primary ownership document for land and property transfers across the province. The stated objective is to reduce fraudulent transfers and provide reliable, verifiable ownership records by linking certificates to the computerized land records system.

Why It Matters

The GPC affects sellers, buyers, legal advisors, banks, and land revenue offices. By tying ownership records directly to a digitized registry, the system aims to make verification quicker and reduce manual errors. For market participants, the presence of a GPC on a title is now an important compliance checkpoint because possession of the certificate will be mandatory for transactions from December 2026.

Recent Developments

Available updates indicate the following rollout timeline and operational developments:

Pilot launch in Sahiwal on May 1, 2026, to test processes and systems.

Progressive operational rollout from July 2026, including payment modes and identity verification steps.

By December 2026, possession of the GPC will be required for all land/property transactions across Punjab.

Online portals, mobile apps, and payment gateway integrations have been introduced to support applications.

Government communications emphasize fraud reduction and property ownership validation.

Investment Snapshot

The GPC is positioned as a measure to improve transactional transparency. Immediate impacts during rollout are focused on administrative adaptation, user education, and technical integration. Market participants should treat GPC compliance as a mandatory document requirement from December 2026 and verify certificate status before finalizing transfers.

Market Analysis

Available commentary and advisory material suggest several potential market implications, without quantified forecasts:

Reduced risk of certain types of property fraud where ownership records are contested, through digitized linkage and identity verification.

Potential efficiency gains in transaction processing where online verification and integrated payment systems are functioning well.

Transitional friction during the initial rollout as stakeholders learn new procedures and district offices implement training.

No public data located on direct effects on pricing, transaction volumes, or penalty structures for non-compliance at the time of reporting; verification is recommended where these matters are critical to a transaction.

Comparison Table

Attribute

Traditional Fard

Green Property Certificate (GPC)

Format

Paper-based land/fard document

Digitized certificate linked to computerized registry

Verification

Manual checks at land revenue offices

Online verification via integrated land records; identity checks through NADRA or equivalent

Fraud prevention

Vulnerable to manipulation or forgery in some cases

Designed to reduce fraud through system linkage and automation

Application

Traditional application through revenue office procedures

Online portals, mobile apps, and payment gateways; nominal fee

Investment Score

The Investment Score for the GPC is qualitative: the certificate suggests improved legal clarity and administrative transparency which could strengthen buyer confidence over time. During the rollout period, investors should expect administrative transition risks and verify GPC status directly through provincial online systems and relevant district offices.

Investment Insight

For buyers and investors, the GPC is primarily an ownership-verification tool. It does not replace the need for standard due diligence such as title searches, physical inspections, and legal counsel. The digitized linkage to Punjab’s land records is intended to make title verification more straightforward, but on-ground confirmation and official checks remain necessary—especially during the initial implementation phase when processes are being standardized.

Buyer Checklist

Confirm whether the property has an issued Green Property Certificate and request the certificate reference or online verification link.

Verify identity and ownership linkage through the Punjab land registry online portal or designated verification tool.

Retain proof of payment for the GPC application if a recent certificate was issued (fee reported around Rs. 950).

Cross-check records with NADRA-based identity verification where appropriate.

Consult legal counsel or a conveyancing specialist to confirm transfer procedures under the new GPC requirement.

Follow up with the relevant district land revenue office for on-ground confirmation, especially for society or block-specific questions.

Pros and Cons

Pros

Cons / Considerations

Digitized records aim to reduce certain fraud risks.

Online verification can speed up due diligence.

Integrated payments and identity checks simplify administrative steps.

Initial rollout may cause administrative delays as systems and users adapt.

Society-level implementation details and timelines were not found in available materials; on-ground verification is recommended.

No public data located on penalties or enforcement specifics after the December 2026 deadline; verify with official sources.

Market Outlook

Current information indicates that the GPC is intended to strengthen the integrity of land records and improve transactional transparency in Punjab. The pilot and phased rollout suggest an implementation approach that privileges testing and capacity-building in district offices. Over time, the degree to which the GPC changes market behaviour will depend on operational reliability, user adoption, and the comprehensiveness of digital records across urban and rural registries.

FAQ

Q: Is the Green Property Certificate mandatory? A: According to available updates, possession of the GPC will be mandatory for all land and property transfers in Punjab starting December 2026.

Q: How do I apply for the GPC? A: The application process has been made available through online portals and mobile apps, along with in-person options at district land revenue offices. Identity verification and payment through designated banks (for example, Bank of Punjab) or online payment methods form part of the application workflow.

Q: What documents and fee are required? A: Available information notes a nominal fee of around Rs. 950 and requires identity verification via NADRA or government-issued ID. Exact document lists should be confirmed with the provincial online portal or the relevant district office.

Q: Does the GPC replace the Fard immediately? A: The GPC is being introduced to replace the traditional Fard for property transfers. The phased rollout began with a pilot in May 2026 and the GPC is expected to be mandatory from December 2026. Specific transition arrangements should be verified with official channels.

Q: How does this affect properties in Multan societies? A: No society-specific implementation details were found in the available material. For Multan areas such as DHA Multan, Royal Orchard, Buch Villas, Citi Housing Multan Phase 1, Wapda Town Phases 1–3, Dream Gardens Phases 1 and 2, PC Colony / Pearl City, Hateem City, Faisal Cottages, Cantt Avenue Society, Model Town / New Model Town, Shalimar Colony, Zikriya Town, and Fatima Avenue / MPS Road belts, general GPC procedures apply. On-ground verification is recommended for society or block-level questions.

Sources and Recent Developments Referenced

The article is based on available government announcements, pilot project reports, news coverage, developer guidance, and advisory materials describing the GPC rollout, pilot timelines (Sahiwal, May 1, 2026), progressive operational steps (from July 2026), and mandatory status from December 2026. Infrastructure updates referenced include integration with the MPDC computerized land records, online portals and mobile apps, designated bank payment links, and NADRA-based identity verification.

Disclaimer

This article is for general information and market awareness only. It should not be treated as legal, financial, tax, or investment advice. Property prices, approvals, possession status, development progress, society policies, and market conditions may change over time. Readers should verify all information from official society sources, government authorities, legal advisors, and on-ground inspection before making any property decision. Zamai Property Partners does not accept liability for decisions made solely on the basis of this article.

Bottom Line

The Green Property Certificate is a significant administrative reform that seeks to digitize and secure property ownership records in Punjab. For buyers, sellers, and advisers, the mandate to possess a GPC from December 2026 makes it an essential element of transaction due diligence. During the rollout phase, confirm certificate status through official portals and district offices and consult legal experts for transfer procedures under the new system.

Conclusion

The GPC initiative reflects Punjab’s move toward a more automated and transparent land administration. While the system is designed to reduce fraud and streamline verification, practical outcomes will depend on the quality of implementation, data completeness in computerized records, and stakeholder adoption. Users should prioritize official verification and remain attentive to further procedural updates from provincial authorities.

Zamai Property Partners Insight

Zamai Property Partners advises market participants to incorporate GPC checks into standard transaction workflows and to request formal online verification links or certificate references when assessing titles. Where society-level specifics are important—particularly in Multan’s varied residential developments—on-ground confirmation from society management and district revenue offices is recommended until comprehensive society-level implementation details are publicly available.

Best Housing Societies in Multan for Investment in 2026

Key Takeaways

Multan’s residential market shows renewed investor interest in 2026, supported by infrastructure improvements and development along the CPEC Western Route. A group of societies stands out in available updates: DHA Multan, Royal Orchard, Buch Villas, Citi Housing Multan Phase 1, Wapda Town Phase 1, Dream Gardens Phase 2, Pearl City (PC Colony), Hateem City, Faisal Cottages, and Cantt Avenue Society near Askari Bypass. Each offers different degrees of maturity, approvals, and lifestyle positioning. Verification on-ground is advised for phases and projects where detailed data is limited.

Quick Facts Table

Society

Approval / Status

Development Status

Notable Feature

DHA Multan

Fully developed, possession-ready

Complete infrastructure

Flagship project; high security and signal-free corridor

Royal Orchard Multan

MDA-approved

Active development

Proximity to South Punjab Secretariat developments

Buch Villas

NOC-approved

Phased construction ongoing

Luxury villas; shorter investment horizons

Citi Housing Multan Phase 1

Established

Fully mature phase with expansion

Located on Bosan Road; mix of residential and commercial options

This article presents a measured overview of leading housing societies in Multan for 2026 investment consideration. The content is derived from compiled, verified updates and recent development notes. It aims to provide an analytical snapshot covering approvals, development maturity, infrastructure links, and relative positioning in the local market. Prospective buyers and investors should treat this as a starting point for due diligence rather than a definitive investment directive.

Why It Matters

Multan’s strategic location along the CPEC Western Route and recent infrastructure activity are contributing to renewed attention from buyers and investors. For individuals evaluating residential opportunities, understanding society approvals, possession readiness, developer reputation, and connectivity is important. Societies with mature infrastructure and credible approvals typically require less short-term verification, while newer or phase-wise projects often require more detailed on-ground checks.

Recent Developments

Recent society-level updates indicate varying stages of readiness across the city. DHA Multan is noted as a possession-ready, fully developed society with extensive infrastructure and a signal-free corridor. Royal Orchard is continuing infrastructure work and benefits from nearby governmental developments. Buch Villas reports phased construction with active deliveries. Citi Housing Phase 1 is expanding into new blocks and commercial zones. Dream Gardens Phase 2 continues phase-wise evolution with gated-community amenities. Hateem City has reported successful balloting events and is progressing facility roll-out. Additionally, DHA has installment schemes reported with four-year plans and initial booking amounts mentioned in recent updates.

Investment Snapshot

Across the societies reviewed, there are a few recurring themes for 2026:

Mature developments (DHA Multan, Citi Housing Phase 1, Wapda Town Phase 1) present established infrastructure and immediate possession options in certain plots.

MDA or NOC approvals are highlighted for several projects (Royal Orchard, Wapda Town Phase 1, Dream Gardens Phase 2, Buch Villas), which may be relevant when assessing legal security.

Gated-community offerings and lifestyle amenities (Dream Gardens Phase 2, Hateem City, Pearl City) are positioned to attract family-oriented buyers.

Emerging locales near Askari Bypass (Cantt Avenue, Faisal Cottages) are marketed for convenient access to upscale areas and existing societies.

Market Analysis

Available updates point to a market environment in Multan that is responding to broader transport and institutional developments. The CPEC Western Route is cited as a strategic factor affecting regional interest. Local market dynamics appear to favor projects with clear approvals and visible infrastructure progress. Societies with possession-ready plots and established road links—such as DHA Multan and Wapda Town Phase 1—are noted as preferred by some local and overseas buyers. Mid-term investment interest is also recorded for MDA-approved projects like Royal Orchard and Buch Villas. For parts of the city where on-ground verification is lacking (for example Wapda Town Phase 2 & 3 and Dream Gardens Phase 1 block-level updates), further inspection is recommended before commitments.

Comparison Table

Criterion

DHA Multan

Royal Orchard

Buch Villas

Citi Housing Phase 1

Wapda Town Phase 1

Dream Gardens Phase 2

Approval

Fully developed / possession-ready

MDA-approved

NOC-approved

Established

MDA-approved

MDA-approved

Infrastructure Maturity

High

Medium-High

Medium

High (mature phase)

High

Developing (gated-community features)

Target Buyer

Security- and possession-focused buyers

Mid-term investors

Buyers seeking luxury villas

Mixed investor and end-user base

Local investors and residents

Buyers seeking gated-community lifestyle

Accessibility

Signal-free corridor and regional links

Close to government developments

Residential pockets

Bosan Road connectivity

Near Northern Bypass

Planned internal connectivity

Investment Score

The following qualitative summary reflects relative characteristics based on verified updates and recent developments. These are not financial recommendations but descriptive categories to help focus due diligence.

DHA Multan: High — mature, possession-ready, widely recognized infrastructure.

Citi Housing Multan Phase 1: High — established phase on Bosan Road with diverse offerings.

Wapda Town Phase 1: Moderate-High — well established with strong local uptake.

Royal Orchard: Moderate-High — MDA-approved, benefits from nearby institutional developments.

Buch Villas: Moderate — NOC-approved, luxury villa focus and phased deliveries.

Hateem City, Pearl City, Faisal Cottages, Cantt Avenue: Developing — positioned for lifestyle and location advantages; require ongoing verification.

Investment Insight

For 2026, a practical approach is to align purchase objectives with society characteristics. If possession readiness and established infrastructure are primary concerns, societies noted as fully developed or mature merit closer review. For buyers focused on gated-community amenities or villa-style living, projects like Dream Gardens Phase 2, Buch Villas, and Hateem City may match preferences but should be assessed for phase-specific delivery schedules. Emerging plots near Askari Bypass could offer location convenience, but their long-term status should be confirmed through on-ground checks and legal verification.

Buyer Checklist

Verify society approval status (MDA/NOC) and obtain official documentation.

Inspect possession availability for specific plots or houses; request official possession certificates where applicable.

Visit the site to confirm infrastructure (roads, drainage, utilities) and surrounding connectivity.

Review developer track record and phase-wise delivery history for phased projects.

Confirm any payment plan terms directly with society offices (for example recent installment offerings reported for DHA).

Seek legal advice on title transfer procedures and lien or encumbrance checks.

Compare competing societies by proximity to schools, hospitals, major roads, and commercial hubs.

Pros and Cons

Pros: Clear approvals for several societies; a mix of mature and developing projects to suit different buyer profiles; improved connectivity cited as a regional tailwind.

Cons: Some phases and block-level details lack verified public reporting and require on-ground verification; detailed pricing and yield figures were not available in compiled updates.

Market Outlook

Available information suggests a cautiously optimistic market environment for Multan in 2026, anchored by infrastructure initiatives and select mature societies that continue to attract buyers. The city presents a range of options from possession-ready flagship developments to lifestyle-oriented gated communities. Given the mixture of mature and developing projects, prospective buyers should focus on documented approvals and visible infrastructure progress as primary selection criteria.

FAQ

Q: Which societies in Multan are possession-ready?

A: DHA Multan is noted as fully developed and possession-ready in available updates. Some plots in mature phases of other societies may be ready, but verification is advised.

Q: Are government approvals available for these societies?

A: Several societies referenced are reported as MDA-approved or NOC-approved (for example Royal Orchard, Wapda Town Phase 1, Dream Gardens Phase 2, Buch Villas). Buyers should request and verify official documents from society or municipal offices.

Q: Is the CPEC Western Route influencing Multan’s real estate?

A: Summarized updates indicate CPEC-related infrastructure developments are a contributing factor to renewed market interest in the region.

Q: Should I consider newer phases or stick to established societies?

A: That depends on your risk appetite and timeline. Mature, possession-ready societies typically reduce short-term delivery risk. Newer phases may offer different amenities but require closer due diligence on delivery schedules and approvals.

Q: Where can I confirm the latest plot availability and payment plans?

A: Contact society offices directly and request official payment plan documents. Recent reports mention four-year installment structures for DHA with lower initial booking amounts, but these should be validated with society representatives.

Sources and Recent Developments Referenced

This article is based on compiled research summaries referencing official society portals, real estate marketing outlets, local news items, social media updates from society and broker accounts, and property listing platforms. Recent development notes cited include possession readiness for DHA Multan, installment plan mentions, phase-wise progress reports for Dream Gardens Phase 2 and Buch Villas, and balloting events and facility updates for Hateem City.

Disclaimer

This article is for general information and market awareness only. It should not be treated as legal, financial, tax, or investment advice. Property prices, approvals, possession status, development progress, society policies, and market conditions may change over time. Readers should verify all information from official society sources, government authorities, legal advisors, and on-ground inspection before making any property decision. Zamai Property Partners does not accept liability for decisions made solely on the basis of this article.

Bottom Line

Multan’s housing market in 2026 presents a mix of established, possession-ready societies and developing gated-community projects. DHA Multan, Citi Housing Phase 1, and Wapda Town Phase 1 emerge as societies with mature infrastructure in available updates, while Royal Orchard, Buch Villas, Dream Gardens Phase 2, Hateem City, Pearl City, Faisal Cottages, and Cantt Avenue offer varying degrees of development and lifestyle propositions. Buyers should prioritize documented approvals, visible infrastructure, and on-ground verification when narrowing options.

Conclusion

Choosing the right society in Multan depends on buyer priorities—possession and infrastructure versus lifestyle amenities and phased project features. The societies profiled here provide a cross-section of the city’s 2026 residential landscape, each with distinct characteristics. A step-wise approach to verification and targeted site visits will help align purchase decisions with individual requirements.

Zamai Property Partners Insight

Zamai Property Partners recommends treating this overview as a curated starting point. For grounded decision-making, combine society-level document checks with on-ground inspections, developer performance reviews, and professional legal counsel. This approach helps balance short-term certainty with longer-term lifestyle and location considerations in Multan’s evolving market.

Real Estate in Multan: Complete Guide to Areas, Societies & Investment Tiers

The Scope of Real Estate in Multan: A Complete Area & Housing Society Guide | Zamai Property Partners

Market Analysis · Multan Real Estate

The Scope of Real Estate in Multan: A Complete Area & Housing Society Guide

Multan has quietly become one of Pakistan’s most interesting real estate markets — not flashy like Lahore or Karachi, but with the kind of steady fundamentals that long-term investors learn to look for.

A growing population, infrastructure investment via the Multan–Sukkur Motorway and Multan Metro Bus, expanding educational institutions, and a meaningful overseas Pakistani diaspora sending capital home have all reshaped the city’s property landscape over the past decade.

For anyone considering Multan property — whether as an investment, a future home, or a hedge for overseas income — the city now offers a tiered market that rewards understanding the geography. This guide walks through what’s actually available, area by area, society by society, and what to watch for before committing capital.

Why Multan, and Why Now

Three trends are quietly compounding in Multan’s favor.

The first is infrastructure. The Multan–Sukkur Motorway has placed the city firmly on Pakistan’s primary north–south trade route. Multan International Airport now handles direct flights to the Gulf, where most of the city’s diaspora lives and earns. Internal connectivity has improved with the Northern Bypass and the Metro Bus, which together have opened up corridors that were rural fringe a decade ago.

The second is demographics. Multan’s population is young, growing, and increasingly urban. Demand for housing — both rental and owned — is structural, not speculative. Educational institutions like Bahauddin Zakariya University, NFC Institute of Engineering, and a cluster of medical and IT colleges keep pulling students and professionals into the city.

The third is capital inflow. Multanis working in the Gulf, Saudi Arabia, the UK, and the US have always sent money home, but property has become the default destination for that capital. A meaningful share of new society plots and ready houses are bought by buyers who live abroad and rarely visit the property in person. This shapes which segments of the market are most liquid.

The result is a market where premium societies command Lahore-adjacent prices in pockets, while emerging corridors still offer genuine entry points for new investors. Understanding the tiers is the whole game.

Multan Property Tiers at a Glance

Area / Society

Tier

Best Suited For

DHA Multan

Premium

Long-term hold, diaspora safety play

Citi Housing Phase 1 & 2

Premium

Branded community, modern lifestyle

Royal Orchard Multan

Mid-Premium

Modern society without DHA-level entry cost

Wapda Town

Mid-Premium

Settled professional families, ready houses

Model Town

Mid-Premium

Established community, walkable amenities

Buch Executive Villas

Mid-Premium

Modern villa living, central location

Gulgasht Colony

Mid-Range

Mature 1-kanal homes, established families

Shalimar Colony

Mid-Range

Built-in community, rental yield

Fatima Jinnah Town

Mid-Range

Established residential, mixed plot sizes

Bahadurpur

Mid-Range

Mid-sized family houses, accessible pricing

Zakariya Town

Entry-Level

Wider plot variety, broader affordability

Northern Bypass Corridor

Emerging

Higher upside, longer time horizon

Fatima Avenue

Emerging

Newer residential corridor, growing demand

MPS Road / Abdali Road / Cantt

Premium

Commercial property, established rental yield

The Premium Tier: DHA Multan and Citi Housing

These two developments dominate the conversation when anyone — especially diaspora buyers — asks about premium Multan property.

DHA Multan sits on the Bosan Road side, well-connected to the city centre and the airport. It carries the Defence Housing Authority brand, which translates into clean documentation, military-backed governance, and consistent maintenance. Plots range from 5 marla up to 2 kanal, with prices commanding the highest per-marla rates in Multan. Sector-by-sector pricing varies considerably — developed sectors with infrastructure and possession trade at multiples of undeveloped or balloted sectors. The risk profile is low and the exit liquidity is high. For overseas Pakistanis who want a “safe” Multan investment, DHA is usually the first conversation.

Citi Housing Phase 1 and Citi Housing Phase 2 are among Multan’s most recognizable branded developments. Phase 1 is the more established of the two, with developed infrastructure, possession largely handed over, and a settled resident population. Phase 2 is the newer expansion, with infrastructure progressing and a longer appreciation runway ahead. Both phases offer modern community planning — wide roads, parks, security, and commercial pockets — and they pull buyers from across Pakistan, not just Multan. The brand recognition keeps demand liquid, which matters when you eventually need to sell. Construction quality and possession reliability have been among the better in Multan’s branded society segment.

Both developments share the same fundamental appeal: brand-backed legitimacy, broad recognition, and the kind of resale liquidity that matters at exit. The downside is the entry price — these are not affordable for a typical first-time investor, and rental yields are modest relative to the capital tied up. They are appreciation plays, not income plays.

The Established Mid-Premium: Wapda Town, Model Town, Royal Orchard, Buch Villas

The next tier comprises the societies that established Multan’s reputation as a serious real estate market in the first place.

Wapda Town Multan was developed for the WAPDA workforce but has matured into one of the city’s most desirable established neighborhoods. The layout is well-planned, the infrastructure is fully developed, the population is settled and stable, and the area enjoys a reputation for being safe, clean, and well-serviced. Prices reflect this maturity. There are fewer empty plots and more ready houses, which makes it a market for buyers who want to live, not just speculate.

Model Town Multan is similar in profile — fully developed, settled, with strong demand from local professional families. Both 1 kanal and 10 marla sizes dominate. The area has seen steady appreciation rather than dramatic swings, which suits the conservative investor or the family genuinely planning to move in. Schools, hospitals, and commercial pockets are all walkable.

Royal Orchard Multan is a newer entrant that has carved out a position between premium branding and a more accessible price point. Possession is well underway, construction quality has been solid, and the location keeps it connected. It’s worth a serious look for buyers who want a modern society without the DHA or Citi Housing premium.

Buch Executive Villas has become a recognizable name in Multan’s mid-premium segment, offering modern villa-style construction in a planned community. The development appeals to buyers who want a ready home rather than the wait of plot-and-construction, and to families who value the security and amenities of a managed community.

These four societies share a profile: established or rapidly establishing, lower volatility, better suited for buyers with a 5–10 year horizon than speculative flippers.

The Local Heart: Shalimar Colony, Bahadurpur, Gulgasht, Fatima Jinnah Town, Zakariya Town

If you want to understand how Multan locals actually live and where established Multani families have owned property for decades, you look at this cluster.

Shalimar Colony is one of Multan’s most well-known older neighborhoods — close to commercial centres, walking distance to several major schools, and home to a deeply rooted community. Plot sizes are mixed, from small 3 and 5 marla plots to larger 10 marla houses. Prices per marla are reasonable relative to the premium societies, and rental yields can be attractive because demand from local renters is consistent. The architecture is varied — some streets have beautifully maintained older homes, others are newer construction. For buyers who want a property in an area with built-in community rather than a half-empty new society, Shalimar deserves attention.

Bahadurpur has emerged as a popular area for mid-sized plots and family houses, particularly on the residential streets branching off the main road. It’s well-connected and has seen consistent demand. Prices are accessible compared to the premium societies, and the area is fully developed with established utilities and services.

Gulgasht Colony is among the older planned neighborhoods of Multan — larger plots, mature trees, established families, and a sense of permanence. It tends to attract buyers looking for established 1 kanal homes rather than empty plots. The neighborhood has held its value because supply is finite and demand from established families is steady.

Fatima Jinnah Town is a long-established residential area with a mix of plot sizes and a settled community feel. It offers the kind of mid-range stability that suits buyers who want a real neighborhood rather than a marketing campaign — schools, mosques, shops, and a network of families who’ve lived there for years.

Zakariya Town, named after the city’s revered Sufi saint Bahauddin Zakariya, is a substantial residential area with broad appeal across income levels. The variety of plot sizes — from compact 3 marla to 1 kanal — makes it accessible to a wider range of buyers, and it has seen meaningful price appreciation over the past several years. Category A plots near the main boulevard are particularly sought after.

These areas collectively represent “real Multan” — neighborhoods where you can buy a property, move in, and immediately be part of a living community rather than waiting years for development.

The Emerging Corridor: Northern Bypass, MPS Road, Fatima Avenue

The most interesting investment story in Multan over the next decade is probably the corridor opening up along the Northern Bypass and adjacent arterial roads.

Northern Bypass plots — particularly commercial frontage — have appreciated substantially as the bypass has become a primary connector. What was once rural land is now commercial corridor with petrol stations, marriage halls, warehouses, and small industrial units. The next phase will likely be planned residential developments feeding off this connectivity. Entry prices are still meaningfully below the established premium societies, which is where the upside lies.

MPS Road (Multan Public School Road) has matured into one of the city’s most desirable commercial and mixed-use addresses. Properties here trade as commercial first, residential second, and command prices that reflect that.

Fatima Avenue and the surrounding pockets have emerged as a newer residential corridor with both plot and house inventory. Connectivity to the main city is improving and pricing remains reasonable.

The thesis for this emerging corridor is straightforward: infrastructure investment usually leads to price discovery with a 5–10 year lag. Multan’s bypass and motorway connections have been built; the property market is still catching up to what that connectivity means for accessibility.

Commercial Multan: Cantt, Abdali Road, MPS Road

For investors interested in commercial property rather than residential, Multan’s commercial heart is concentrated along a few well-established corridors. The Cantt area, Abdali Road, and MPS Road carry the highest commercial rents and the highest entry prices. Yields are stronger than residential premium societies, but the entry capital is significant and tenant management becomes a real consideration. The bypass commercial plots discussed above are the more accessible entry point for someone building a commercial portfolio gradually.

What to Actually Watch Out For

Multan’s real estate market — like all Pakistani property markets — rewards skepticism. A few honest things to keep in mind before signing anything.

Society legitimacy varies enormously. DHA, Citi Housing, Royal Orchard, Wapda Town, and the well-established old neighborhoods are not the issue. The issue is the dozens of smaller “societies” that have launched over recent years with aggressive marketing, partial NOC approval, and unclear timelines. Some will mature into legitimate developments. Others will not. Before buying in any society that isn’t on the established list above, ask for the NOC status from the Multan Development Authority, the master plan approval, and the development timeline in writing.

Plot files versus possession plots are different markets. A “file” you buy today might be a real plot in three years — or might not. The premium goes to plots with confirmed possession and developed infrastructure. If you’re buying for capital appreciation specifically, files can outperform — but only if the society delivers. Diaspora buyers especially should be cautious here because verifying status from abroad is difficult.

Always verify ownership history. Property fraud — fake fards, double-sold plots, encroached land, undisclosed court cases — is the single biggest risk in Pakistani real estate. Before paying anything substantial, get the registry papers verified independently, ideally by a lawyer who has no relationship with the seller or dealer.

Be honest about exit liquidity. Premium societies and established neighborhoods sell quickly when you want out. Plots in emerging societies or marginal locations can sit on the market for a year or more. Match your time horizon to the area’s liquidity profile.

Negotiate. Always. Listed prices in Multan, as in most of Pakistan, are usually starting points. Serious buyers consistently transact 5–15% below the initial asking price, particularly for plots sitting unsold or sellers in a hurry.

Where the Smart Money Is Going

If you were to summarize Multan’s real estate scope in one paragraph, it would be this: the established premium societies offer safety and steady appreciation at high entry prices, the older settled neighborhoods offer real community and reasonable yields, and the emerging corridors offer the highest upside with proportionally higher risk. The right answer depends on your time horizon, your appetite for verification work, and whether you intend to live in the property or hold it from a distance.

For overseas Pakistanis, the conservative playbook is one premium society plot (DHA or Citi Housing) as a long-term hold, paired with an established neighborhood house (Wapda Town, Model Town, Buch Villas, or Shalimar) for either family use or rental income. For local buyers building wealth from a smaller base, the emerging corridors and Zakariya-tier areas offer real entry points where capital can still appreciate meaningfully.

Multan isn’t going to surprise anyone with a 200% boom year. But that’s not the city’s profile — it’s a market that compounds steadily for buyers who do the work. And that, over a decade, is usually how the most successful property portfolios get built.

Looking for verified Multan properties?

Every Zamai listing is independently checked. Members get full disclosure on title, history, and any concerns before bidding.

This article is intended as a general overview of Multan’s real estate landscape and is published for informational purposes only. It is not investment advice, legal advice, or a recommendation to buy, sell, or hold any specific property. Property market conditions, prices, society approval status, and development timelines change frequently and vary by individual plot and seller.

Before committing to any property transaction, readers are strongly encouraged to conduct independent verification of title, ownership history, NOC approval, and society legitimacy through qualified legal counsel and the relevant regulatory authorities including the Multan Development Authority. Zamai Property Partners is committed to transparency on every property we list — but no article, including this one, replaces the due diligence each buyer must do for themselves.

References to specific housing societies, areas, and developments are based on publicly available information and our general market observation. Inclusion in this guide does not constitute endorsement, nor does omission imply any negative assessment.

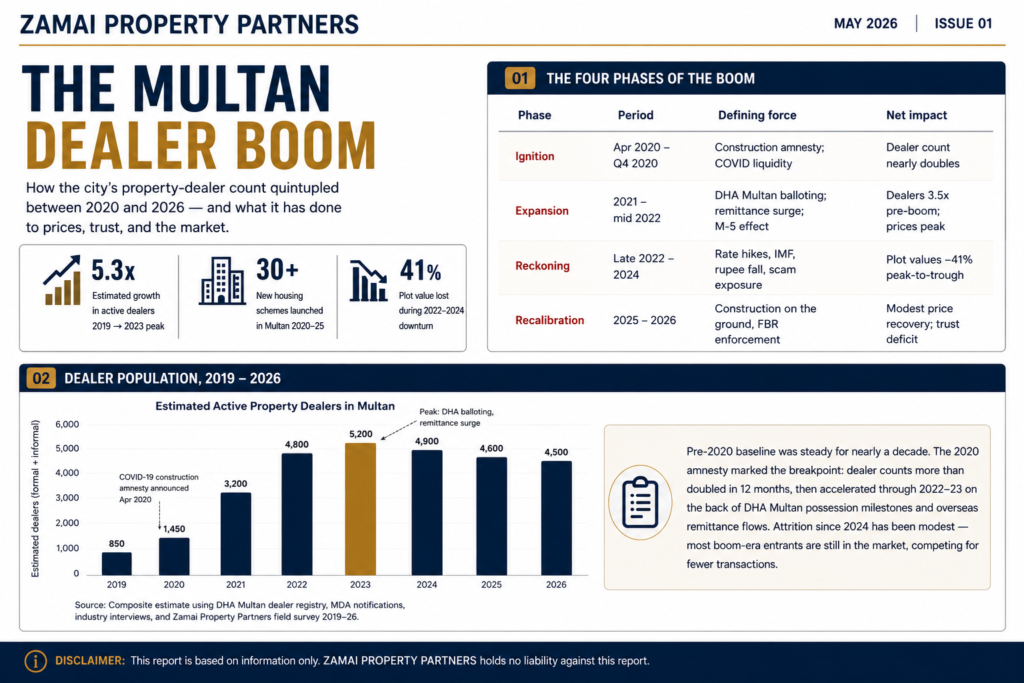

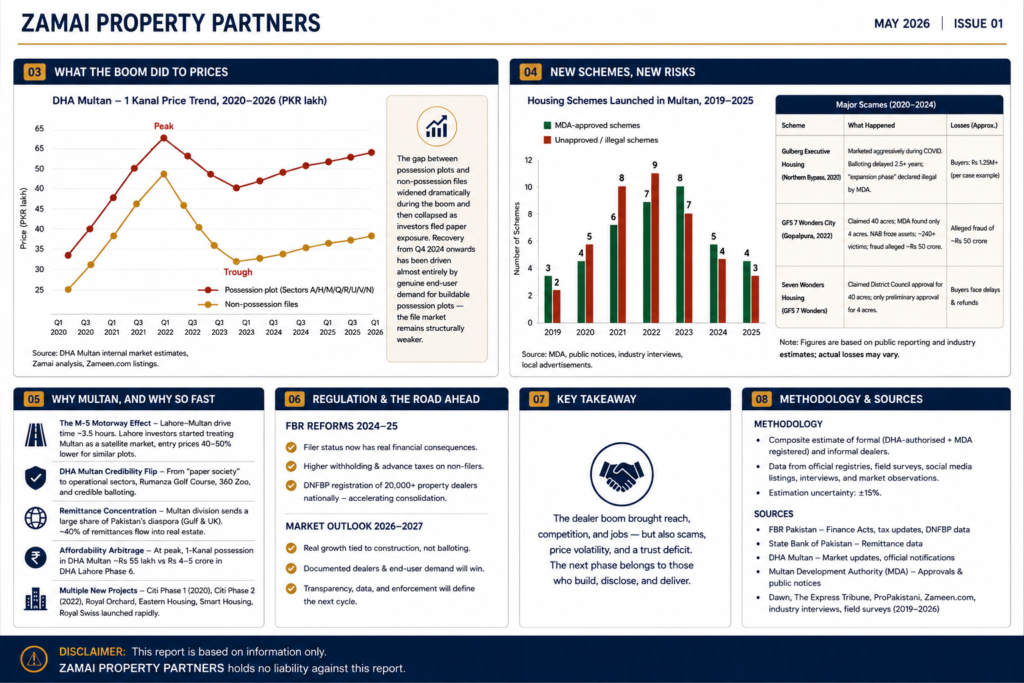

The Multan Dealer Boom: How the City Got 5,000 New Property Offices in Six Years — and What It Broke

By Zamai Property Partners · May 2026 · 6 min read

Between 2020 and 2026, something unusual happened in Multan’s real estate market. If you spent any time on Bosan Road, Northern Bypass, or around the expanding commercial strips near DHA Multan, you would have noticed it almost immediately. Property offices seemed to appear overnight. What was once a business dominated by a relatively small circle of established agencies suddenly became crowded with consultants, brokers, freelancers, social media agents, and self-styled real estate advisors. In just a few years, property dealing in Multan shifted from a specialised profession into something that almost anyone seemed willing to try.

A decade ago, the local property market felt much smaller and far more predictable. Buyers generally knew the names of serious agencies, and most transactions happened through offices with established reputations. Many firms had been operating for years, sometimes generations, and trust played a major role in how business was conducted. That landscape has changed dramatically. Today, a polished office is no longer the standard marker of credibility. Some dealers operate from commercial plazas, others from shared desks, and some have no physical office at all, relying entirely on WhatsApp, Facebook, or YouTube to attract clients.

The turning point was 2020. COVID disrupted traditional businesses and pushed many people to look for alternative income sources. At the same time, Pakistan’s construction sector incentives created renewed excitement around real estate investment. Multan happened to be well positioned for that wave. DHA Multan was beginning to show real development progress, the M-5 Motorway improved connectivity, overseas remittances remained strong, and multiple housing schemes were launching aggressively. For many people, real estate looked like the easiest opportunity available, and property dealing became the preferred entry point.

What followed was not gradual growth but a rapid explosion. People who had never worked in real estate began facilitating small deals, earning commissions, and deciding to stay in the business. Informal brokers emerged everywhere—friends connecting buyers to sellers, part-time consultants chasing leads, and newcomers trying to build credibility through social media. The barriers to entry were almost non-existent. A smartphone, confidence, and a few property videos were often enough to start appearing legitimate.

Social media accelerated the transformation. Before this period, property sales in Multan were largely relationship-based, with trust built through personal connections and local reputation. After 2020, visibility became the new currency. Younger dealers embraced YouTube walkthroughs, TikTok clips, drone footage, and Facebook marketing far faster than traditional firms. Suddenly, a person sitting in Multan could generate inquiries from Karachi, Lahore, Dubai, Toronto, or Birmingham without ever meeting a client face to face. In many cases, digital presence began to replace professional credentials in the minds of buyers.

To be fair, not all of this change was negative. The newer generation brought energy and modern marketing practices to a market that had often felt outdated. Presentation standards improved. Response times became faster. Multan’s property sector gained wider visibility, especially among overseas Pakistanis. But the same accessibility that encouraged innovation also lowered standards. When anyone can enter a profession overnight without training, licensing, or accountability, the quality of market participants inevitably becomes inconsistent.

By late 2021 and into 2022, the market felt unstoppable. Plot prices were rising, investors were flipping files quickly, and new housing projects kept entering the conversation. Confidence was high, perhaps unrealistically so. In such an environment, people stop asking whether prices are sustainable and start assuming growth will continue indefinitely. That mindset fed the dealer boom, because when everyone believes transactions will keep happening, everyone wants a share of the commissions.

The correction, when it came, was harsh. Rising interest rates, inflation, higher construction costs, tax pressures, and weakening speculative confidence slowed the market significantly. The easy-money phase ended, and the difference between genuine businesses and temporary operators became obvious. Established firms survived because they had systems, repeat clients, and reputations to protect. Informal operators often vanished just as quickly as they had appeared. Buyers who had trusted branding or aggressive sales pitches discovered that some “agencies” were little more than short-term setups.

Perhaps the biggest damage was not purely financial, but reputational. Trust in the profession took a major hit. When buyers repeatedly encounter exaggerated claims, manipulated pricing, unclear approvals, or disappearing agents, they become sceptical of everyone—including honest professionals. That trust deficit still affects the market today. Serious agencies continue to operate responsibly, but suspicion has become a natural starting point for many buyers.

The rapid expansion of loosely regulated selling also created opportunities for poor-quality or questionable projects to gain traction. Buyers often assumed that if multiple dealers were promoting a scheme, it must be credible. That assumption proved costly in many cases. Approval status, possession claims, and development timelines became areas where buyers needed far more caution than many initially realised.

By 2026, the market feels more grounded. It is no longer driven by the same speculative enthusiasm, but it is not collapsing either. Real development activity in stronger projects has helped restore some confidence. DHA Multan’s possession sectors show actual residential construction, educational institutions are contributing to end-user demand, and investors appear more selective than they were during the peak years. That is a healthier environment overall.

Still, the dealer overhang remains. Many individuals who entered the market during the boom are still active, competing for fewer transactions in a more cautious environment. That pressure can encourage shortcuts, aggressive selling, or misleading positioning. Buyers today need to be far more deliberate than those who entered during the hype cycle.

The Multan dealer boom left behind a mixed legacy. It modernised marketing, created employment, expanded visibility, and brought fresh energy into the city’s real estate sector. But it also increased noise, weakened trust, and made it harder for ordinary buyers to distinguish between professionals and opportunists. Both realities exist at the same time.

The most practical lesson for buyers remains simple: verify the person, not just the project. A professional-looking social media page is not proof of credibility. Ask questions, visit offices, cross-check approvals, compare rates, and be cautious of urgency-driven sales tactics. In today’s market, patience is often more valuable than speed.

At Zamai Property Partners, we believe real estate should be transparent, documented, and professionally handled. Whether you are buying, selling, or simply trying to understand where the market stands, informed decisions matter more than ever.

How to Buy a Plot in Multan — What Nobody Tells First-Time Buyers

Buying property in Multan for the first time? Before you sign anything, read this. We cover everything from choosing the right area to verifying documents — so you don’t lose your hard-earned money.

Content:

Let me be straightforward with you. Multan’s property market is full of opportunity, but it is also full of people who will take advantage of a buyer who does not know what they are doing.

According to Punjab Land Records Authority (PLRA) data, over 47,000 property transactions were registered in Multan district in 2024, a 23% jump from 2021. More buyers, more transactions, and unfortunately, more disputes. Property fraud cases in Punjab rose by 18% between 2022 and 2024, with Multan among the top five affected districts.

The good news is that most of these problems are completely avoidable.

Fix Your Budget Before You Look at Anything

Sellers and agents want you to fall in love with a plot first and figure out the money later. Do not do that.

As of early 2025, here is where Multan plot prices generally stand. A 5 Marla plot runs between PKR 35 and 80 lakh. A 10 Marla plot falls somewhere between PKR 70 lakh and 1.8 crore. A 1 Kanal plot starts around PKR 1.5 crore and goes well above 4 crore depending on location.

These numbers shift based on area, road width, corner position, and whether utilities are connected. But the bigger issue most buyers miss is what comes on top of the plot price. Stamp duty is 3% of the property value. Registration fee is another 1%. If you are a non-filer, CVT adds 2% more. Agent commission is typically around 1%, and development charges vary by scheme.

In total, add 8 to 10% on top of whatever price you agree on. If you have not budgeted for this, you will have a serious problem on registry day.

Know Why You Are Buying

This sounds obvious but most buyers skip it, and it costs them.

If you are buying to live there, your priorities should be sewerage, gas connection status, distance from main roads, and schools nearby. A plot that is cheap because it has no gas line or sits on a narrow gali will affect your quality of life every single day.

If you are buying as an investment, look at areas that are still developing but have clear growth indicators such as nearby government projects, new road infrastructure, or proximity to an established scheme. Over the past three years, areas along Northern Bypass and adjacent to DHA Multan have shown consistent price appreciation. Mature areas like Model Town and Gulgasht offer stability but lower upside.

Neither approach is wrong. But mixing them up is where people get stuck.

Documents — This Is Where Most Buyers Get Hurt

Do not let anyone rush you through this part.

The most important document is the Fard. It confirms who the legal owner of the property is right now. Get it fresh from PLRA, either at their office or online at plra.punjab.gov.pk. A Fard is only valid for 15 days, so make sure yours is recent. If a seller hands you an old Fard, that is a red flag worth taking seriously.

The previous sale deed shows you the chain of ownership. Check that the name of the current seller matches exactly with what is on the Fard. Even a minor spelling difference can cause problems at the sub-registrar office.

If the plot is in a private housing scheme, it must have a No Objection Certificate from the Multan Development Authority. Many schemes in and around Multan operate without one. Buying in an unapproved scheme is a risk most buyers only understand after something goes wrong.

The Khasra and Khatoni numbers are the official land identification numbers. Cross-check them against the PLRA online record yourself. Do not just take the agent’s word for it.

An Encumbrance Certificate confirms there is no loan, lien, or legal dispute against the property. Your lawyer can get this from the sub-registrar office. It costs very little and takes a day or two. It is worth it.

Visit the Plot More Than Once

A location pin and a few photographs tell you almost nothing.

Go to the plot yourself. Bring a measuring tape or hire a local surveyor. It costs PKR 2,000 to 3,000 and confirms the plot dimensions match the documents. Check whether boundary markers are in place or if a neighboring structure is encroaching on the land.

Visit at different times of day. Walk around the area. Talk to people who live nearby. They will tell you things no agent ever will, whether it is water supply issues, flooding during monsoon, or disputes with the scheme developer.

Negotiate Without Showing Your Hand

In Multan, the asking price is a starting point, not a final number. Most sellers leave a 5 to 15% gap for negotiation.

Before you make any offer, research what similar plots in the same area have recently sold for. When you sit down to negotiate, point to specifics like an unpaved access road, no gas connection, or distance from the main road as reasons to go lower. These are legitimate factors and sellers know it.

The biggest mistake in negotiation is letting the other side know you have already decided. Once they sense urgency, the price stops moving.

Token Money — Get Everything in Writing

Once you agree on a price, token money locks the deal and takes the plot off the market. This is usually 2 to 5% of the total price.

Whatever you pay, get a written receipt immediately. It should include the exact amount, the date, the plot details, a deadline for completing the transfer, and the seller’s CNIC number. Also agree in writing on what happens if either side backs out. Pay by cheque or bank transfer. For large amounts, cash creates problems later when you need a paper trail.

Registry Day

The final transfer happens at the sub-registrar office. Both buyer and seller must be there in person with original CNICs. Bring a fresh Fard not older than 15 days, the original previous registry, both parties’ original CNICs, two witnesses with their CNICs, and stamp paper of the correct value based on the property price.

Once the registry is done, collect your original document and keep it somewhere safe. Scan it and store a digital copy as well.

What Catches Buyers Off Guard

Buying in an unapproved scheme because it was cheaper. Paying the full amount before registry is complete. Trusting one agent completely instead of verifying independently. Skipping a lawyer to save PKR 10,000 and then spending ten times that fixing a problem later. Not asking about the area’s flooding history, which matters more than most buyers expect in parts of Multan.

None of these mistakes are unusual. They happen to careful people every year. The only real protection is slowing down and checking everything yourself.

Property in Multan is a genuine opportunity right now. Prices have risen but demand continues to grow, from within the city and from overseas Pakistanis. The buyers who do well here are not the ones who move fastest. They are the ones who know what they are looking at.

At Zamai, every property goes through verification before listing, and our auction model means you see real bids in real time with no guessing what someone else paid. If you have questions about a specific area or property, reach out.